- Fri. Apr 26th, 2024

Latest Post

JPMorgan CEO Warns of Potential Stagflation as High Inflation Plagues U.S. Economy

JPMorgan CEO Warns of Potential Stagflation as High Inflation Plagues U.S. Economy

Newest Gas Station Chain Makes Its Mark in Irmo: Murphy Oil Corporation Takes Over Harbison-Area Wells Fargo Bank Property

Newest Gas Station Chain Makes Its Mark in Irmo: Murphy Oil Corporation Takes Over Harbison-Area Wells Fargo Bank Property

From Humble Beginnings: Omaha Public Schools’ Bluestem Middle School Robotics Team Makes VEX World Championships Debut

From Humble Beginnings: Omaha Public Schools’ Bluestem Middle School Robotics Team Makes VEX World Championships Debut

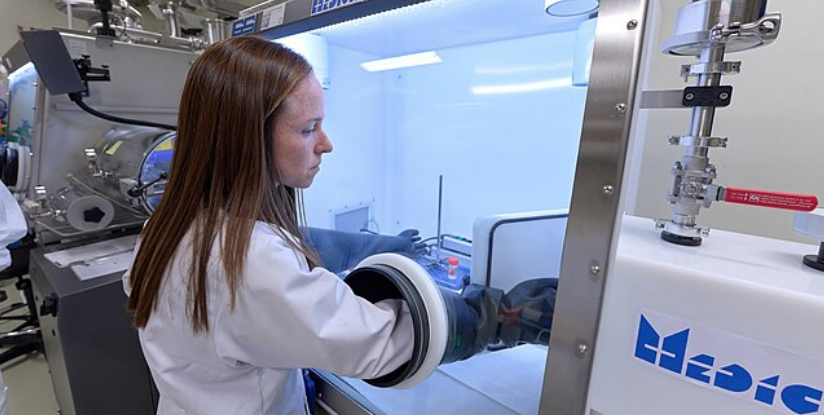

The BIOSECURE Bill: A Controversial Proposal to Isolate US Pharmaceutical Companies from Chinese Economic Interactions and its Implications for the Healthcare Sector

The BIOSECURE Bill: A Controversial Proposal to Isolate US Pharmaceutical Companies from Chinese Economic Interactions and its Implications for the Healthcare Sector

JPMorgan CEO Jamie Dimon Warns of Potential Stagflation as Federal Reserve Takes Action on High Consumer Prices

JPMorgan CEO Jamie Dimon Warns of Potential Stagflation as Federal Reserve Takes Action on High Consumer Prices

JPMorgan CEO Warns of Potential Stagflation as High Inflation Plagues U.S. Economy

JPMorgan CEO Jamie Dimon has expressed caution about the U.S. economy and the potential for stagflation as high consumer prices continue to plague the country. In an interview with The…

Newest Gas Station Chain Makes Its Mark in Irmo: Murphy Oil Corporation Takes Over Harbison-Area Wells Fargo Bank Property

The Irmo area has seen the addition of a new leaseholder as Murphy Oil Corporation takes over a previously occupied Wells Fargo Bank property. The company, which operates over 1,700…

From Humble Beginnings: Omaha Public Schools’ Bluestem Middle School Robotics Team Makes VEX World Championships Debut

Omaha Public Schools’ Bluestem Middle School is sending a team to the VEX Robotics World Championships for the first time in about a decade. Coach Sheri Cohen Vollmer has been…

The BIOSECURE Bill: A Controversial Proposal to Isolate US Pharmaceutical Companies from Chinese Economic Interactions and its Implications for the Healthcare Sector

The growing trend to isolate the US from Chinese economic interactions has led to a proposal to prevent US drug companies from outsourcing tasks to Chinese firms. This could have…

JPMorgan CEO Jamie Dimon Warns of Potential Stagflation as Federal Reserve Takes Action on High Consumer Prices

JPMorgan CEO Jamie Dimon recently cautioned about the U.S. economy, expressing concern that stagflation could be a potential outcome as the Federal Reserve works to control high consumer prices. In…

Celebrate Women’s Empowerment at Fort Worth’s Women’s Market – Sip & Shop on April 28th!

On Sunday, April 28th, Fort Worth will be hosting a free event to celebrate women-owned businesses. The Women’s Market – Sip & Shop is being organized by Women Who Collab,…

Align Technology Repurchases $150 Million of Its Own Common Stock: Boosting Shareholder Value Through Ongoing Stock Buyback Program

Align Technology (Nasdaq:ALGN) has announced its plans to repurchase $150 million of its own common stock as part of its $1 billion stock repurchase program approved in January 2023. This…

Brazilian Soccer Legend Marta Announces Retirement from International Soccer: Leaving a Legacy and Pursuing New Opportunities

Brazilian soccer legend Marta, currently playing for Orlando Pride, has announced her retirement from international soccer this year. At 38 years old, she holds the record for Brazil’s all-time leading…

ByteDance Stands Firm Against TikTok Ban: Will US Users Say Goodbye to Their Favorite App?

TikTok, the popular video-sharing app, is facing a potential ban in the U.S. due to national security concerns about the Chinese government’s ability to access U.S. user data through the…

Eagles A.J. Brown Extends His Contract by Three Years, Secures $80 Million with New-Money Average of $32 Million per Year

Receiver A.J. Brown has signed a three-year contract extension with the Eagles, which guarantees him $80 million and makes him the highest-paid receiver in terms of new-money average, earning $32…